UK wage growth falls sharply, raising hopes of interest rates cuts on horizon

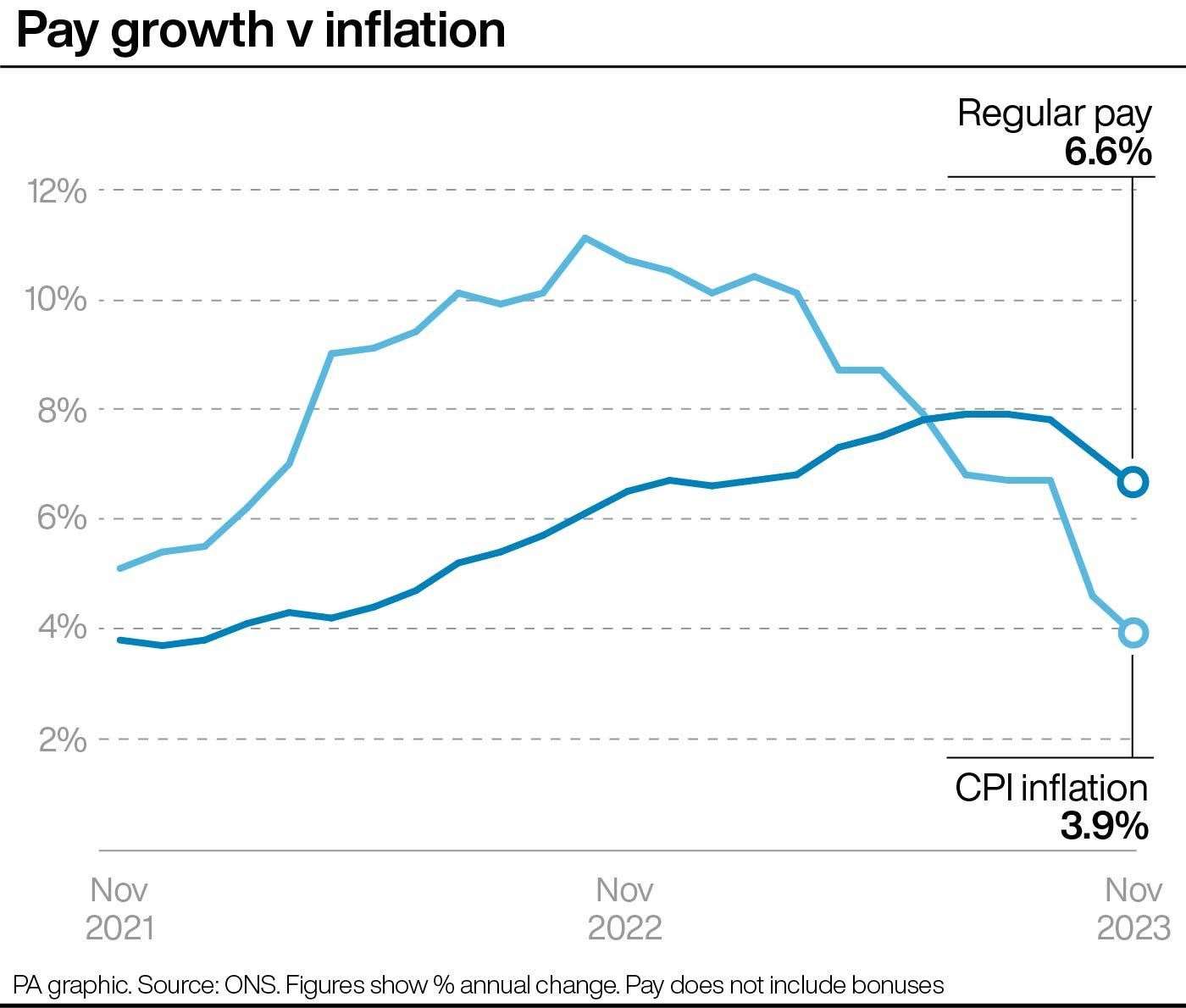

Wage growth in the UK has slowed to the lowest rate for 10 months, reinforcing hopes that the Bank of England could consider cutting interest rates as the jobs market continues to cool.

But official figures also revealed that earnings have outstripped price rises for the fifth month in a row, in a boost to workers amid the cost-of-living crisis.

UK average regular earnings, excluding bonuses, increased by 6.6% in the three months to November, down from a revised 7.2% in the previous three months, the Office for National Statistics (ONS) said.

It is the lowest rate since the three months to January last year and one of the steepest falls in earnings growth since during the pandemic.

The latest data could give Bank of England policymakers further reassurance that higher interest rates are working their way through the economy, reinforcing expectations that they will begin cutting borrowing costs later this year.

Craig Erlam, senior market analyst for Oanda, said that inflation has fallen faster than expected and with wage growth slowing sharply, “there is every chance we see much more over the coming months that enables the Bank of England to pivot towards cutting interest rates”.

“It is probably a little early to expect too big a pivot but it could lay the groundwork for a May cut as long as the data continues to comply,” he added.

James Smith, developed markets economist for ING, said “the bottom line is that both wage growth and services inflation, the datasets that are guiding monetary policy right now, are below Bank of England projections”.

But he said the Bank will want to see more evidence that pay growth is easing and wage expectations among firms has come down before “kick-starting” rate cuts.

However, when taking into account the effect of Consumer Prices Index (CPI) inflation, pay lifted 1.4% over the latest period.

It means that real wages have been rising since July, as UK inflation has eased.

Chancellor of the Exchequer Jeremy Hunt said: “It has been tough for many families recently, but with inflation now falling and the economy gradually returning to growth, today’s continuing rise in real wages will offer further relief.

“On top of this the cut in national insurance contributions will get more people back into the jobs market, not just supporting economic growth but saving a typical two-earner household around £1,000 this year.”

Meanwhile, the number of job vacancies fell by 49,000 over the three months to December to 934,000, marking the 18th period in a row that openings have fallen and the longest run of falls ever recorded.

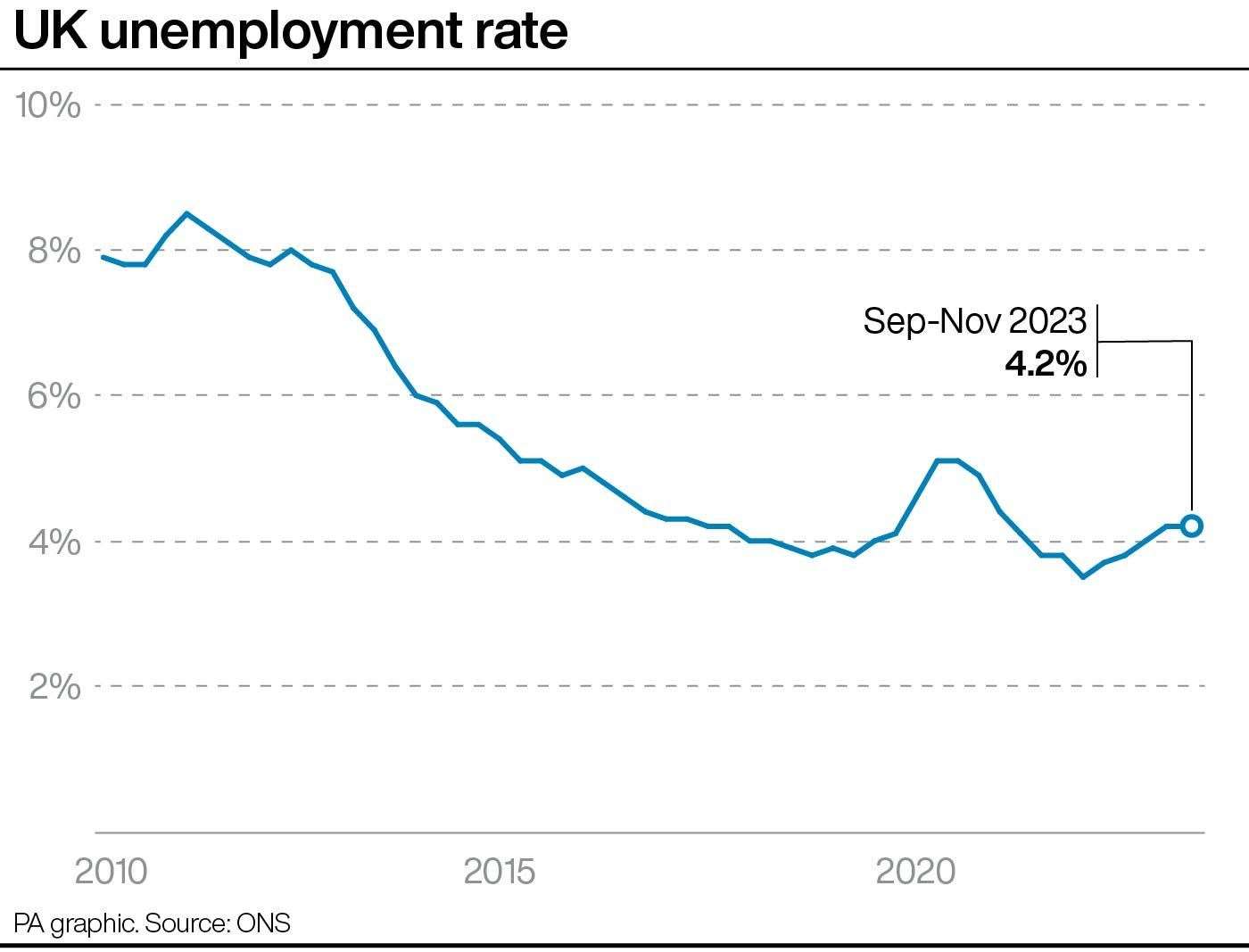

The rate of UK unemployment remained unchanged at 4.2% in the three months to November.

But more real-time data showed the number of UK workers on payrolls fell by 24,000 to 30.2 million for December, compared with November, although the ONS cautioned this was subject to revision.

The wider jobs data, which is being collated using extra data sources to estimate the figure due to low responses to its labour force survey, showed that the rate of UK employment increased to 75.8% from 75.7% in the previous quarter.

Liz McKeown, the ONS’s director of economic statistics, said: “The overall picture continues to be broadly stable, with the unemployment rate unchanged and the employment rate up slightly on the previous three months.

“While annual pay growth remains high in cash terms, we continue to see signs that wage pressures might be easing overall.”

Hannah Slaughter, senior economist at the Resolution Foundation, said that 2023 was “a year of two halves for pay packets, with strong growth in the first six month of the year, and barely any growth at all after the summer”.

She added: “This means that annual pay growth will continue to fall in early 2024 – and is no longer fuelling inflation.

“With the labour market continuing to cool, the big question is at what level pay growth will stabilise – and what this mean for the health of workers’ real wages.”

Read more

More by this author

PA News